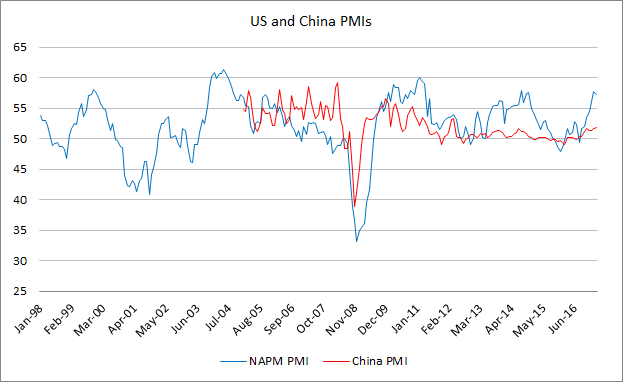

From 2004 till 2008, US manufacturing (as measured by the NAPM PMI) has been weak, before diving in 2008. Since then it has rebounded and fallen into a range of 50 – 57, steady if not robust expansion.

In China, manufacturing was flourishing pre 2008, after which it declined steadily from over 55 to below 50 in 2011. It has flirted with 50 since then until early 2016 when the China went into QE lite mode and resuscitated the economy.

2016 appears to be the year of a synchronized global manufacturing recovery. Even chronically troubled economies such as Europe and Japan witnessed a rebound in PMIs around mid 2016.

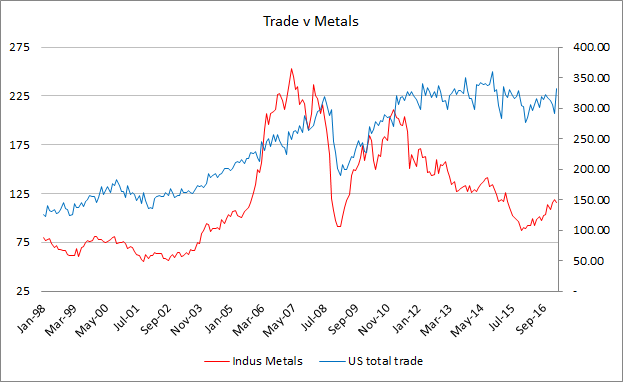

Before 2008, US trade policy was dominated by efficient production with the current account relegated to a state variable. From 2009, with most avenues blocked, the US, and indeed most countries in the world, attempted to export their way out of recession. The result was trade peaking in late 2013, early 2014.

A consequence of this Cold Trade War was a recession in manufacturing and industrial commodities. In 2016, global manufacturing had re-adjusted itself to more domestic facing production. This has been responsible for some of the recovery in manufacturing and the recovery in commodities.

How far can the current recovery extend before it once again meets the limits of decreased trade?

For the US, PMI’s fell as productive capacity was offshored pre 2008. From 2010, PMI’s have been supported by reshoring. However, loss of trade is also a loss of productive efficiency. Eventually, trade stagnation will lead to loss of productivity and to falling output growth. The question is how long the gains of reshoring can persist before inefficiencies set in.

*all data sourced from Bloomberg.